Apply

Fill out this simple application

Consultation

1-on-1 business consultantion

Funding

Funding as soon as 7 days

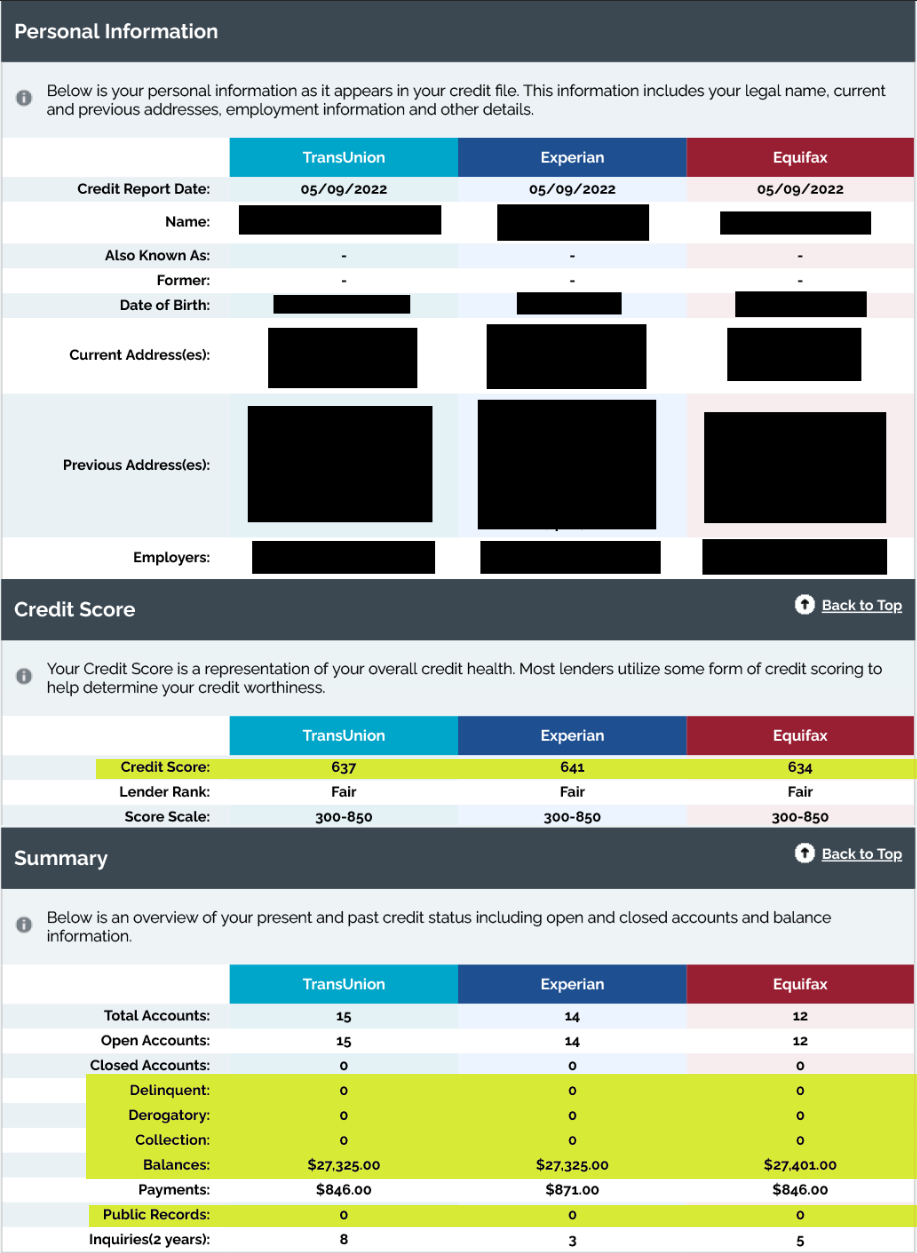

On May 9, 2022, I had a consultation with a prospective client. He was interested in going through our business credit card program. Unfortunately, his credit scores were not high enough to qualify.

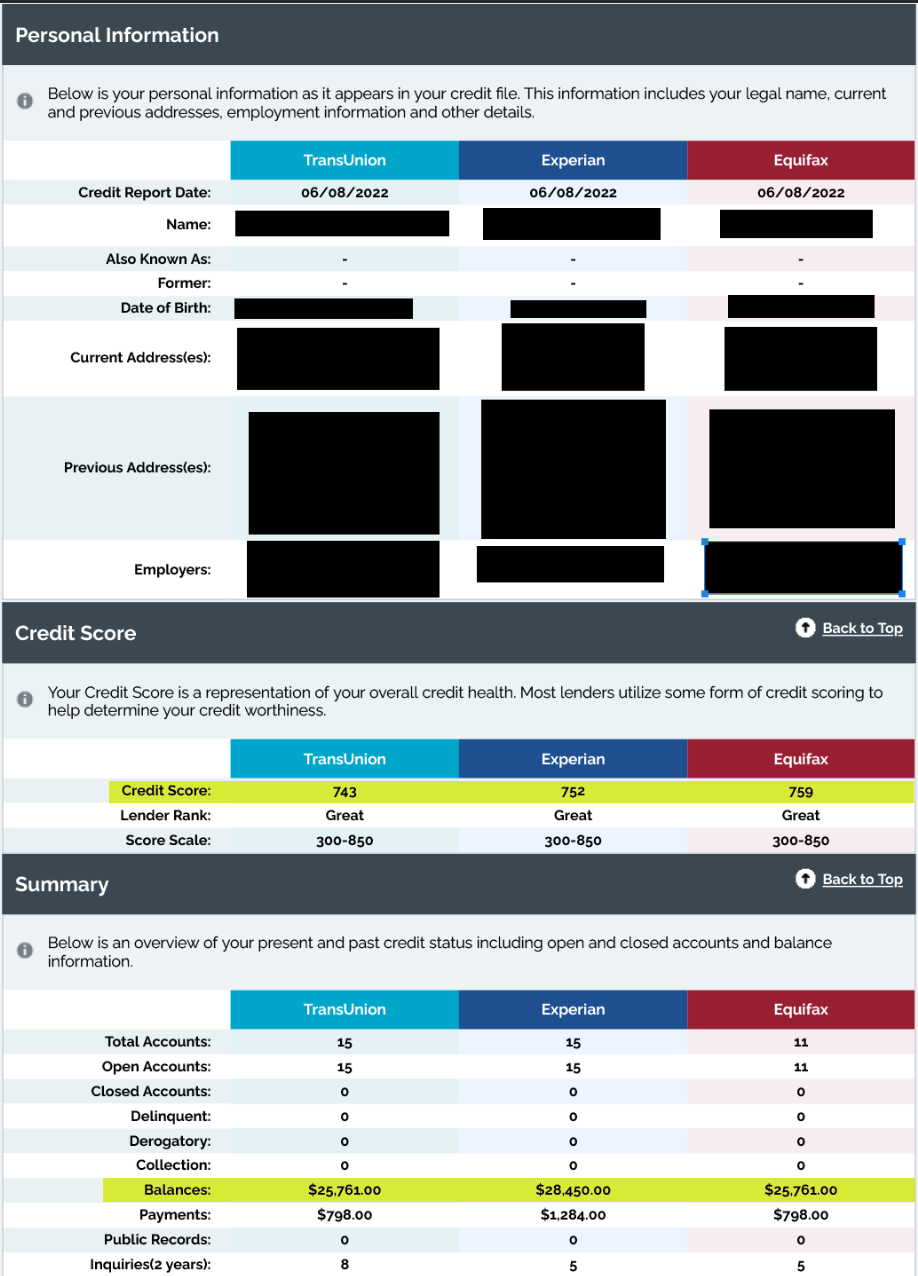

He told me about how his business is growing fast and he can get a very high return if he had additional capital to invest. I can sympathize with his situation. Most of the clients that we serve are in the same boat as this client. On 5/9/22, he had an average credit score of 637.

The crazy thing about this client was the fact that he has NEVER been late on any payments or defaulted on any debt.

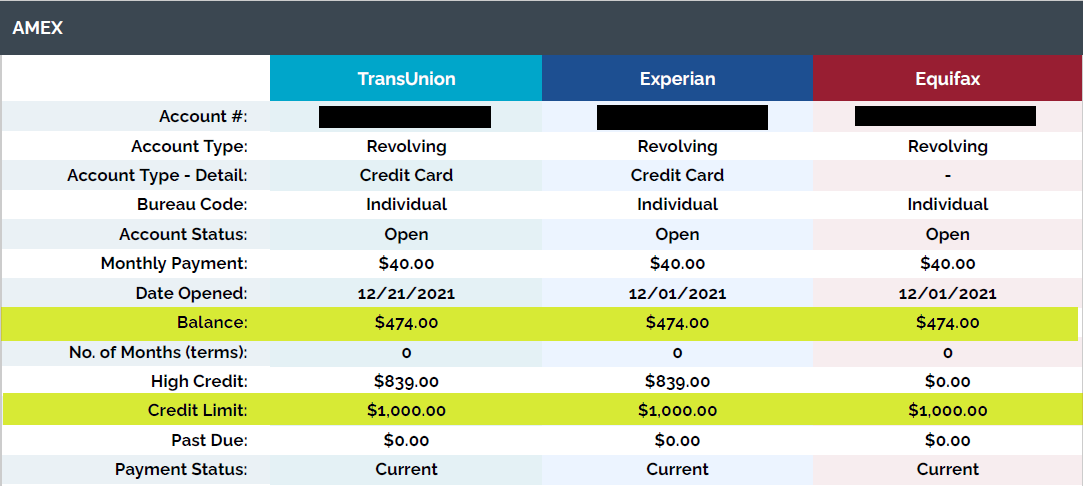

Here’s a snapshot of the report:

So what was causing the low credit score? Let’s dive a little deeper. There were over a dozen open accounts reporting on his credit, including this teeny-tiny revolving account.

The account in question:

I had a sneaking suspicion that the client’s score was artificially low because he was over the limit on his AmEx card by only $20. It turns out the client had just opened the card and used it for some business expenses. He used the entire amount because it had a 0% intro rate and then accidentally went over the limit on the last purchase he made.

I gave the client a game plan to strategically pay down these personal credit cards and we would have a follow up conversation in a month.

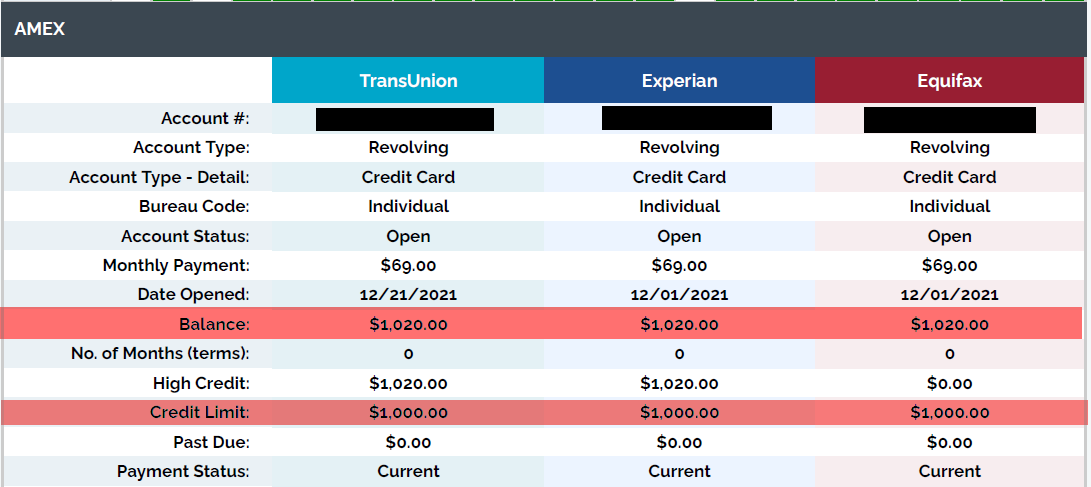

Below is the snapshot:

Although the total amount of debt on his report didn’t change much, the teeny-tiny Amex account was paid down to below 50%.

As you can see, the Amex has been paid down: