Apply

Fill out this simple application

Consultation

1-on-1 business consultantion

Funding

Funding as soon as 7 days

Today I want to break down and establish why an 800 credit score is completely different than a brand new 800 credit score, and I’m going to show you what the differences and I’m going to show you five factors that you need to focus on instead of the score itself.

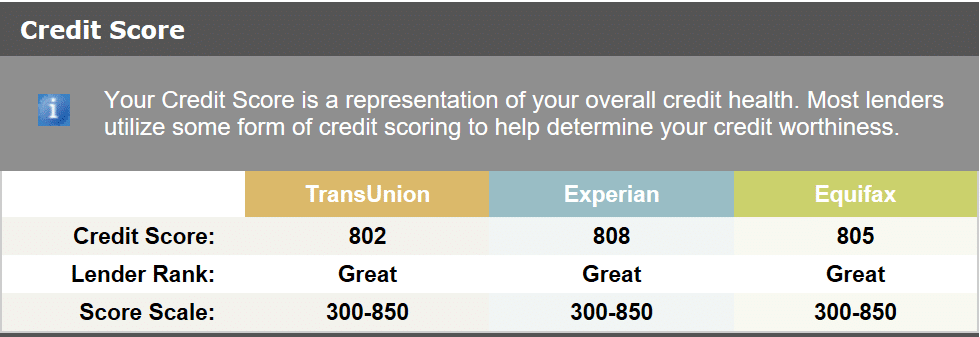

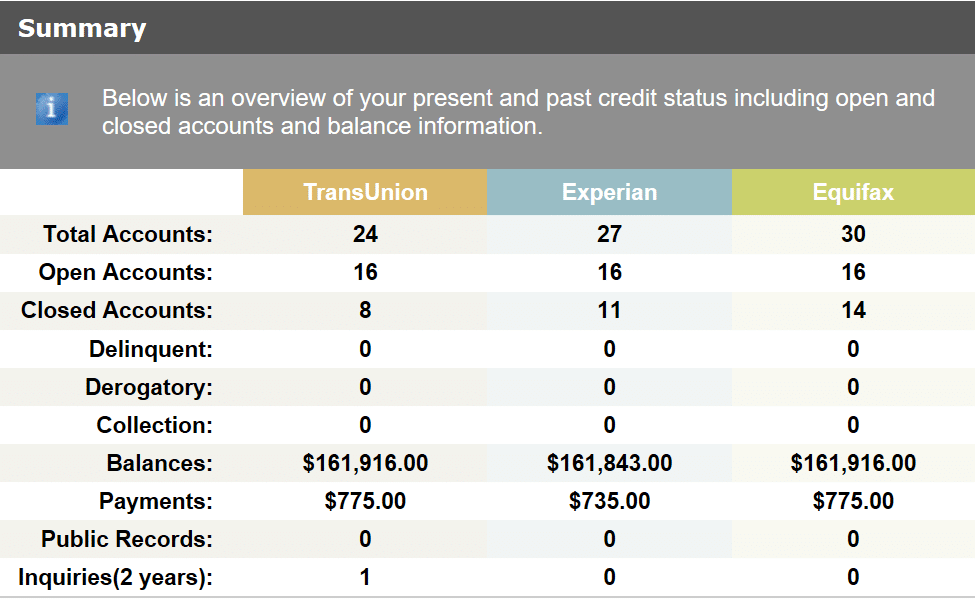

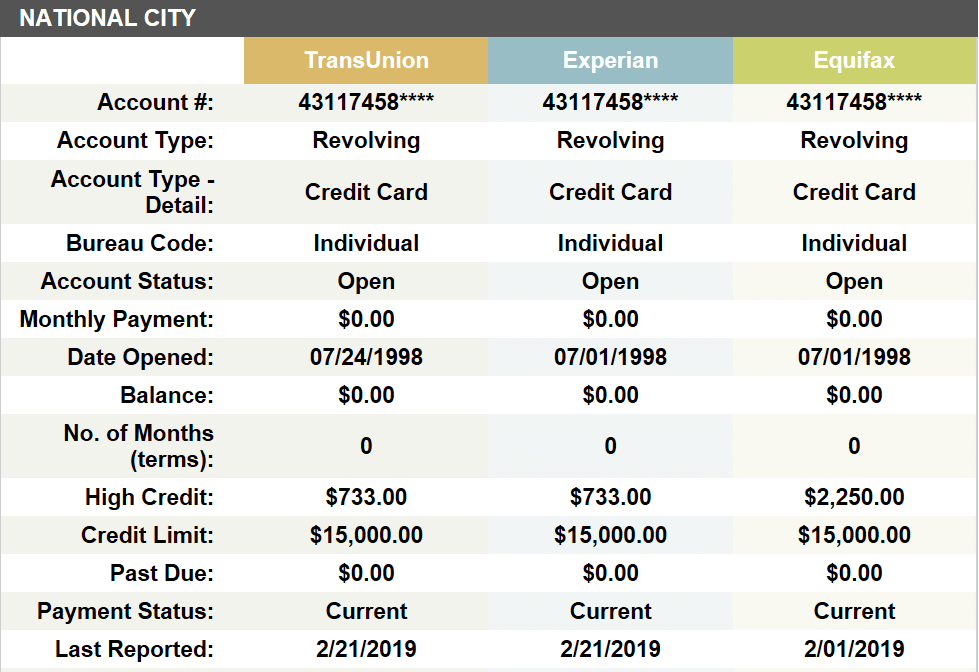

So take a look at this first credit report. It says that he’s got 802 808 and 805 credit scores, excellent credit by any standard, however he only has two years of credit history and only got three accounts a store card, a student loan, and an authorized user account that belongs to one of his parents that they let him use. If he were to miss a payment or get a late-payment his 800 credit score on average would probably tumble down all the way into the 750 just by having one 30-day late payment because he doesn’t have enough credit history.

This bring us to a major flaw in our FICO system you can artificially have a high credit score just by having a short excellent payment history.

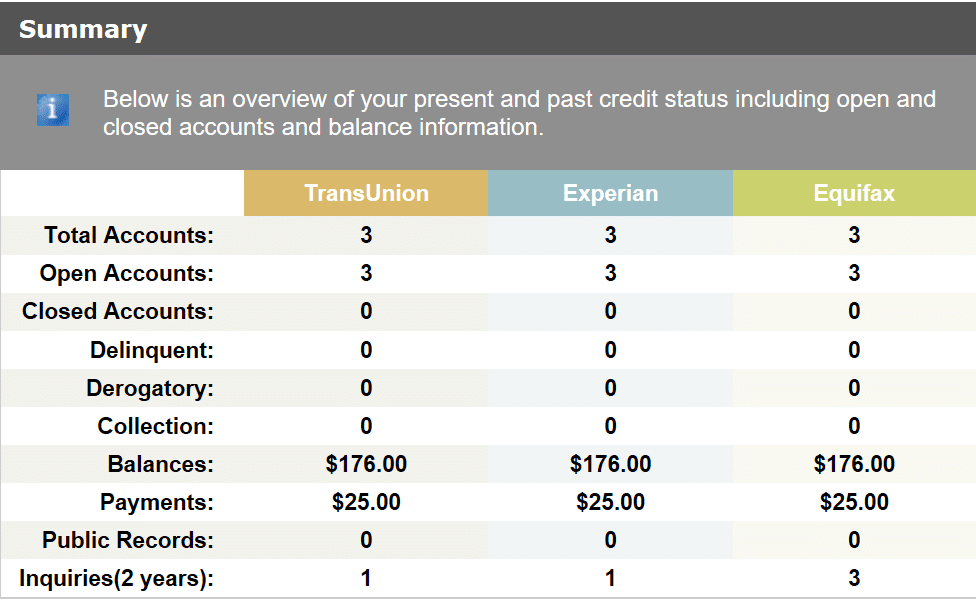

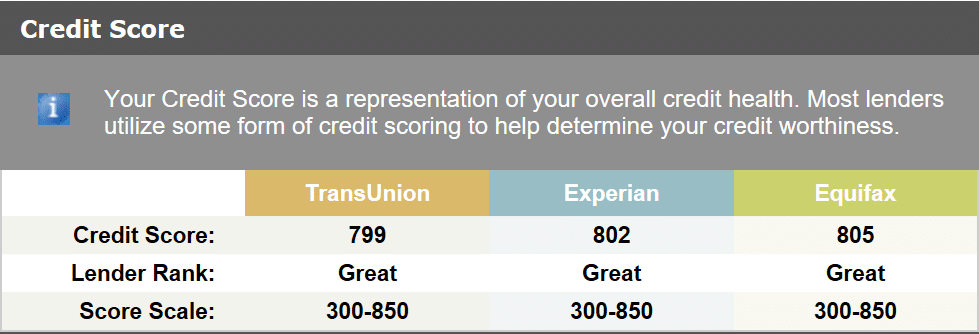

Now let’s look at another credit report that is a little bit older, he is in his forties and he’s got also 790 802 805 credit very very respectable scores. Excellent payment history he’s never missed a payment before in his entire life, and he has 20 years of credit history, and 16 accounts. If he was to get a 30-day late his score might only be impacted maybe 5 or 10 points as opposed to 50 or 60 are young entrepreneur friend so as you could see there’s a lot of other factors that matter when it comes to credit score next we’re going to cover what factor is and what to look for instead of the actual credit score.

5 Factors that matter more than your credit score

Let’s go through them 1-by-1

- Payment History

- Amount Owed

- Length of Credit

- Types of Credit

- New Accounts & Inquiries

1 thought on “800 FICO vs 800 FAKO”

I see the value given and please keep the videos coming! I’m applying Monday was waiting on my monthly update from identityiq.com Shout out to PK and Rafael V.