Apply

Fill out this simple application

Consultation

1-on-1 business consultantion

Funding

Funding as soon as 7 days

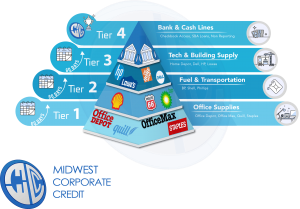

Just like your personal credit profile and score, your business has it’s own credit profile and score. This infographic breaks down the different tiers in building your company’s credit profile.

When your business has little or no credit, you will want to start small. Think back to when you were in your early 20’s and had no personal credit. You probably started off with store cards with low limits. Perhaps a $300 Macy’s card. After a few months of on time payment history on this account, perhaps you were offered a higher limit on this card or another card with a different retailer. A few months later, you upgraded to secure bank credit card. Once these 3-4 accounts built your credit score, you were offered an unsecured Visa or Mastercard with a small limit. Then you got your first car loan. Then eventually your first mortgage.

Building Business credit is no different than the process you used to build your personal credit. Just like any other endeavor, there are short cuts to building your business credit. This roadmap will guide you in building a solid business credit profile within 6-8 months.

2 thoughts on “Building Business Credit”

Does your business have to show income before getting approved for the checkbook business lines of credit?

Hi Winston,

Yes, your business must have at least two years of operating history, as well as documented income to be approved for a business checkbook line of credit. Don’t let the attractiveness of a physical checkbook blind you to the other great funding options your business can leverage for massive growth! If your business is pre-revenue, then our Startup Funding Program is a great option for you, and you’ll find that you can use the funding just as conveniently as you would an actual checkbook.

I’d be happy to send you more information on both programs, or schedule a time for one of our Business Growth Consultants to speak with you about your funding options.

–Dan