Published 8/8/2016 – Author: ‘The Team at Midwest Corporate Credit’ – Providing modern day education and solutions for your contemporary financing needs

–

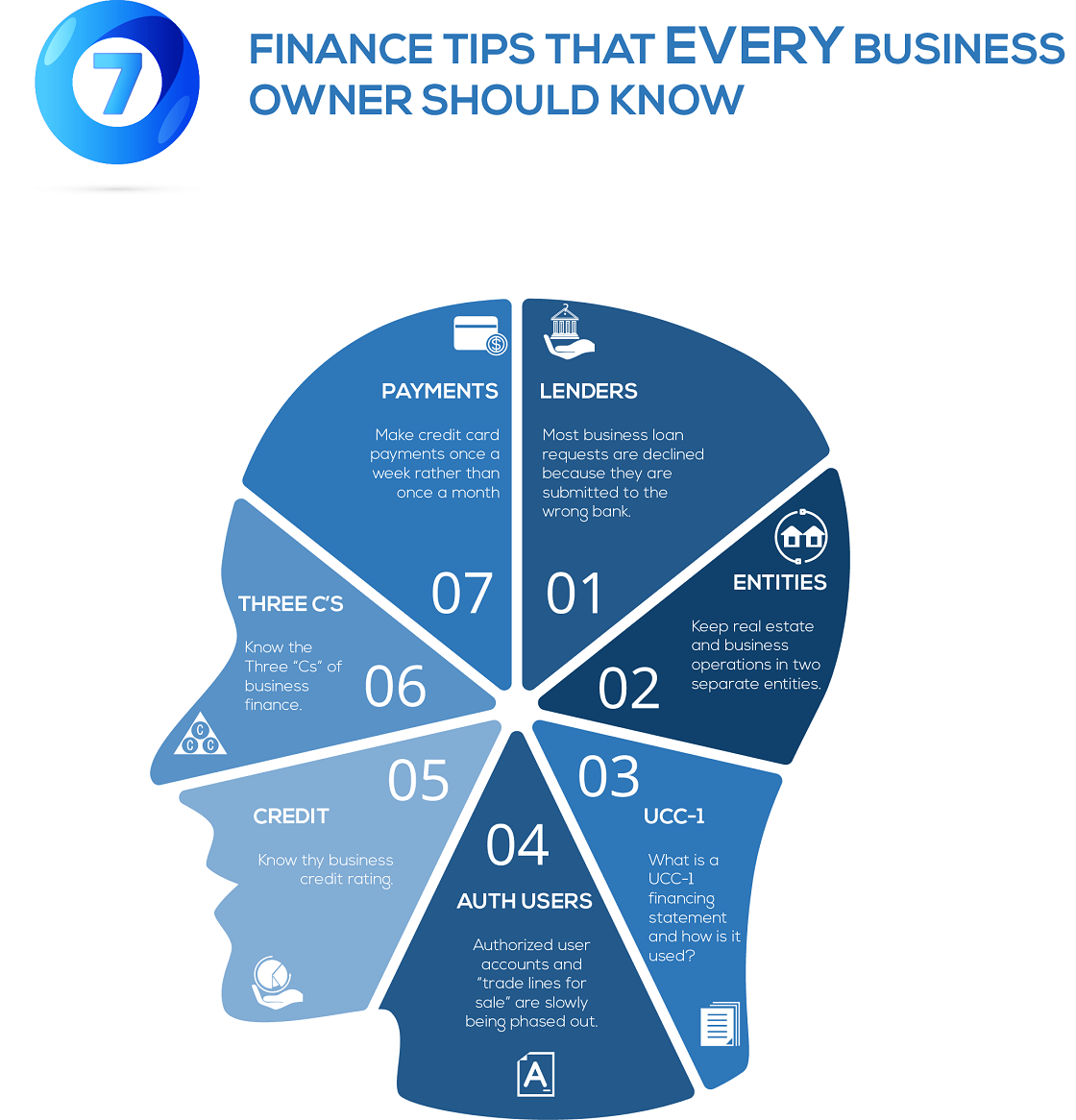

1. Make credit card payments once a week rather than once a month

Credit card issuers report balances to the credit bureaus once a month. By making weekly payments rather than monthly payments, a lower credit card balance will be reported on your credit report. For example, let’s say you have a credit card with a $10,000 limit and you charge $8,000 on it every month. At the end of the month, you pay off the $8000. If that credit card has a reporting date that’s closer to the end of the month when your balance is the highest, it will always reflect that the card is 80% utilized. This will cause a low credit score. Instead, if you pay $2000 per week, the balance will always be 20% and therefore will always report on the credit report as being only 20% utilized. This will result in a higher credit score!

2. What is a UCC-1 financing statement and how is it used?

A UCC-1 (Universal Commercial Code-1) financing statement is a legal document that a creditor will file with the secretary of state to protect his interest against any pledged collateral that the debtor owns. A UCC-1 is just like a mortgage except its used for other assets that the business owns instead of real estate. Some examples of collateral are receivables, vehicles, equipment, etc…. Yes, it’s that simple!

3. Keep real estate and business operations in two separate entities.

Keeping your business operations in a different corporate entity than your real estate in which the business runs out of will have multiple benefits:

- When applying for a business loan, business operations are easier to underwrite due to lack of real estate exposure.

- Multiple SBA loans are easier to obtain due to the existence of multiple entities.

- Having two different entities will offer superior asset protection. (Please check with a licensed attorney on this point)

- It would be easier to sell one of the assets without disrupting the operation of the other.

4. Most business loan requests are declined because they are submitted to the wrong bank.

A business owner should know the difference between a commercial bank and a retail bank. In general, commercial banks are business friendly and will typically have underwriting guidelines that are more liberal. A business owner can set themselves up for successfully obtaining business financing by forming a relationship with 2-3 commercial banks when the business is new.

5. Know the Three “Cs” of business finance.

Cash: Like the old saying goes “cash is king.” Having liquid cash on hand sends a message to the banker/ underwriter that the company is well capitalized and risk of insolvency is minimal.

Credit: We believe that this is the most important of all the “Cs.” Credit gives the banker/ underwriter a direct look at the business and it’s owner’s financial habits and character. Past financial history is a good indication of how the borrower will service the current loan request if granted.

Collateral: Having collateral to pledge in exchange for a loan lowers the lender’s risk of loss. If the loan goes into default, the lender is entitled to repossess the asset that was pledged and liquidate it to recover the loan proceeds.

In conclusion, the more cash, higher credit, and more collateral a business has, the higher the chances of a loan approval and loan better the loan terms.

6. Know thy business credit rating.

Most business owners don’t realize that their business has a credit rating just like they have a FICO score as an individual. There are several business specific credit bureaus that lenders use to underwrite a business loan request. Some major bureaus are Dun & Bradstreet, Corporate Experian, and Commercial Equifax. The credit bureau that a creditor will review a report from depends on the size of the business, industry, and the type of creditor (bank, credit union, B2B supplier, etc…)

7. Authorized user accounts and “trade lines for sale” are slowly being phased out.

What is an authorized user account? It is simply a credit account that a family member or a friend owns that they add you on to. The theory is that the history of that account will cause an instant surge in your credit score when it reports to your credit. In the last few years credit bureaus and credit issuers have caught on to this loophole. The new FICO 08 scoring model will eliminate such accounts from the FICO score. Additionally, some banks have already stopped reporting history of these accounts to the credit reports of authorized users.